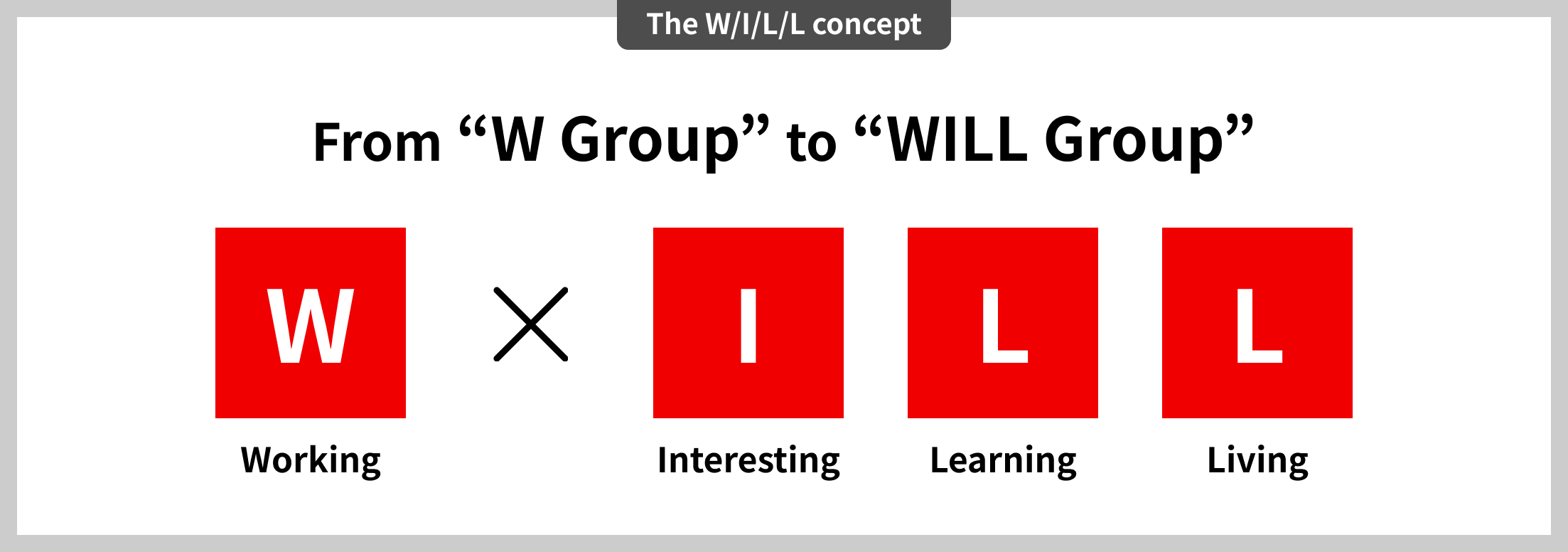

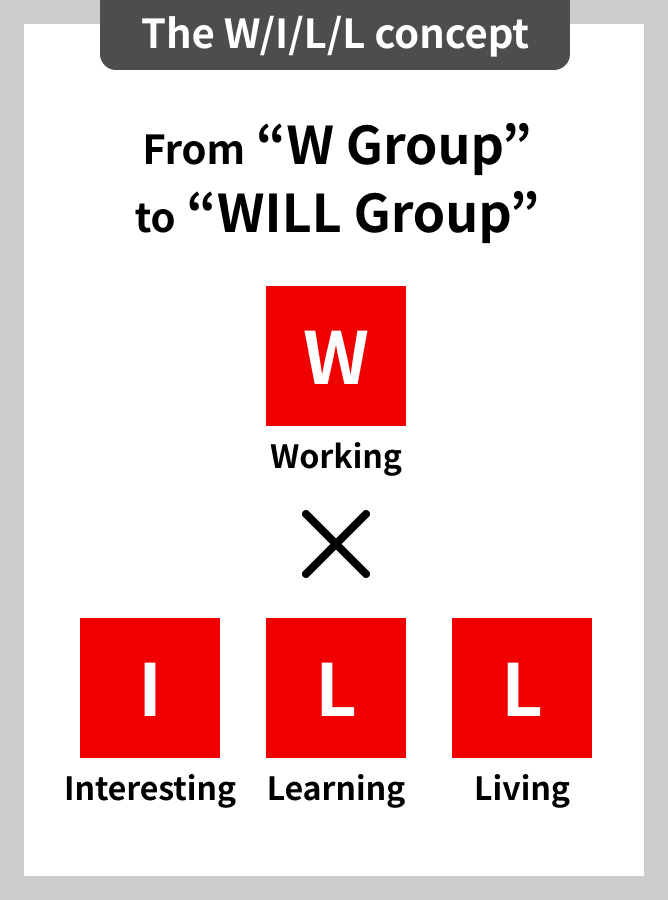

Toward the medium to long term : From “W Group” to “WILL Group”

In May 2026, the Group formulated a new Medium-term Management Plan (WILL-being 2029).

In preparing this plan, management spent over a year in discussions, asking, “What do we want to achieve?” and “What kind of company do we want WILL Group to be?”

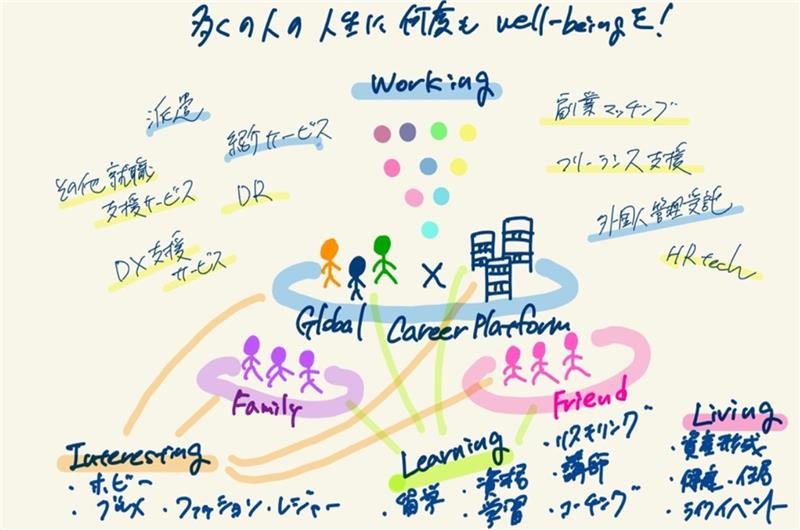

I am somewhat reluctant to show this because it is a rough sketch, but this is my hand-drawn vision of the WILL Group’s future.

With this drawing, we began discussion on what we want the WILL Group to look like in the future.

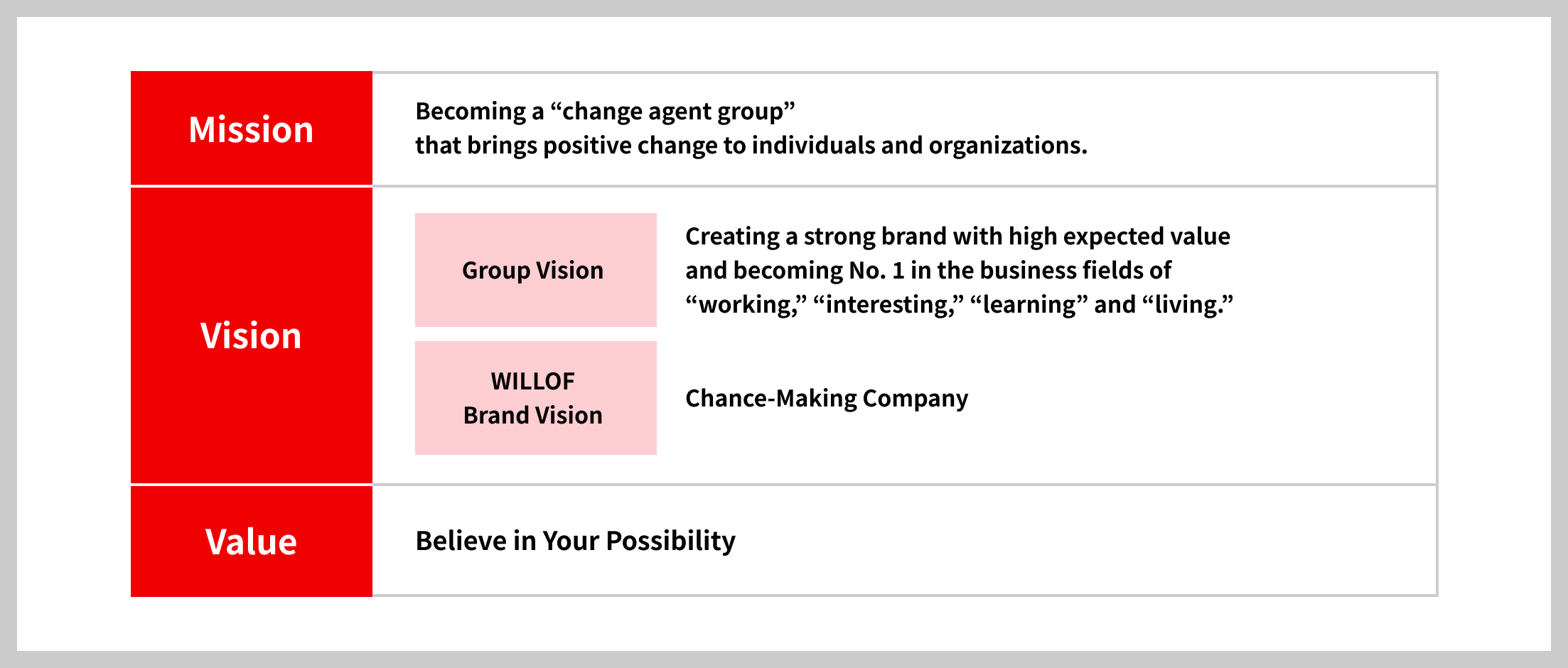

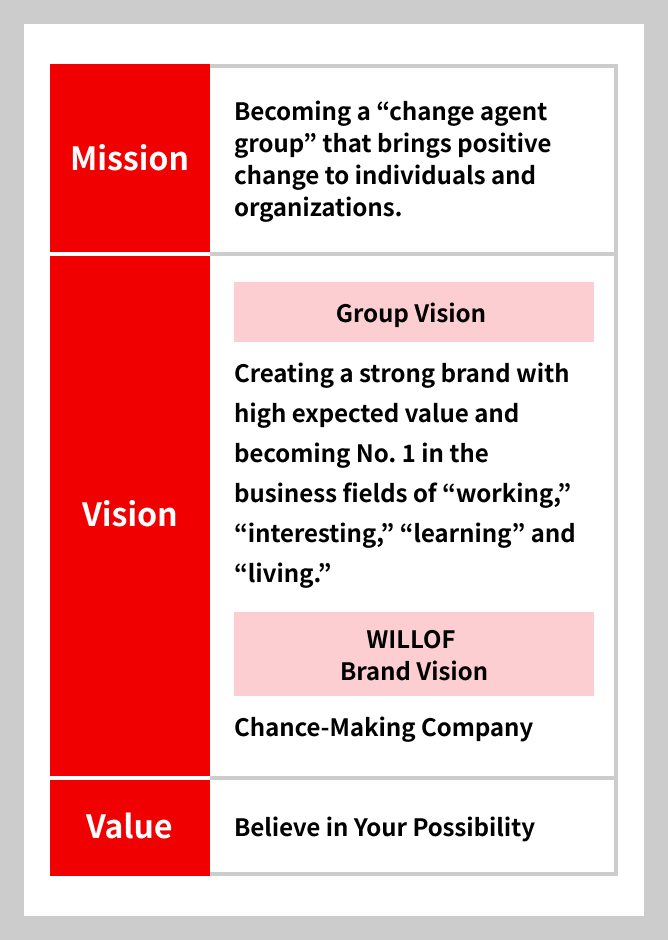

Although each officer expressed it differently, the image of the WILL Group that everyone aimed for was rooted in our Mission, Vision, and Value (MVV).

Twenty years have passed since we established our MVV, and the area that currently diverges most from the ideal is the Vision.

In the 30 years since our founding and 20 years since we established our Vision, we have achieved growth by focusing solely on Working Business. In that sense, we are a “W” group. The WILL Vision entails deploying business that contributes to achieving our mission not only in the domain of W: Working, but also in the domains of I: Interesting, L: Learning, and L: Living.

We have thus established our theme toward the medium to long term as transitioning From “W Group” to “WILL Group.”

The state we aim to achieve—From “W Group” to “WILL Group”—is one where Working Business remains at the core, and the I/L/L businesses exist to enhance its social value, which equals business value.

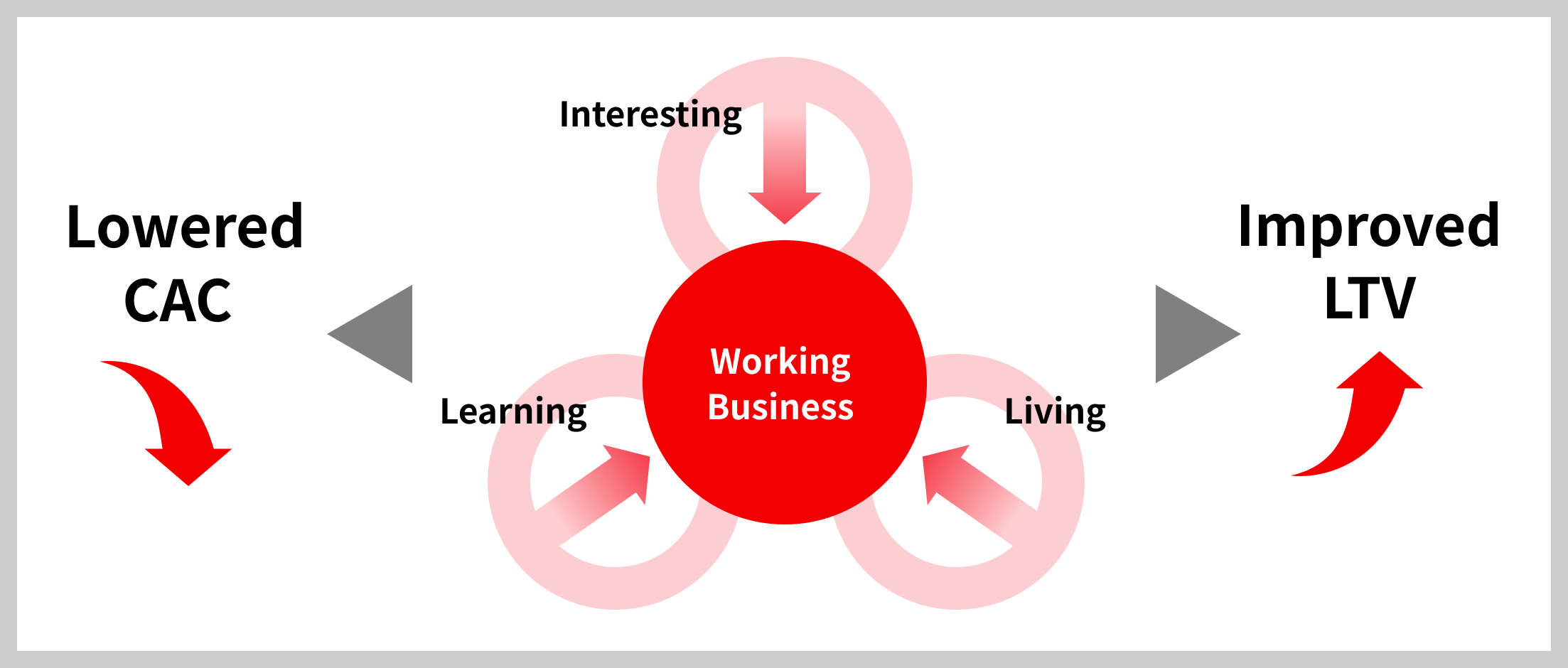

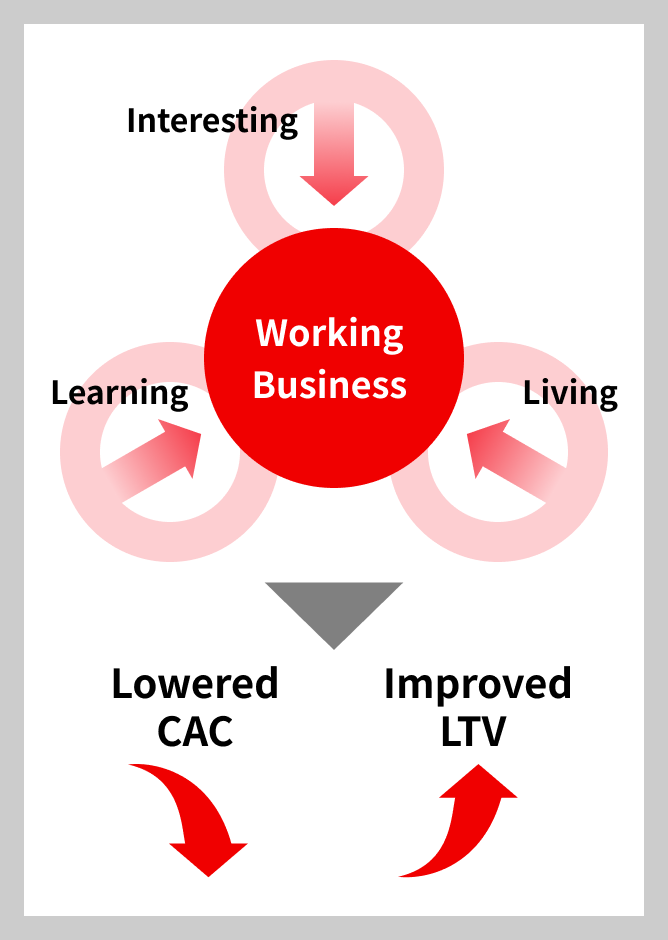

WIn the W business environment, the most important metrics are Life Time Value (LTV) and Customer Acquisition Cost (CAC). These metrics are directly linked not only to job seekers (workers) but also to companies (workplaces).

In addition to the immediate hiring challenges, difficulty in securing new business for companies is likely to increase in the future, making LTV/CAC management even more critical for both job seekers and companies. How can involvement by the Group increase LTV for both people and companies? How can we address the ever-increasing CAC? These are challenges shared not only by us but by the entire human resource services market.

To overcome these challenges, the Group has implemented various measures within the Working Business domain, including operational and compensation improvements. Moving forward, in addition to these efforts, we aim to resolve this challenge by leveraging the I/L/L business domain to drive improvements in LTV for both job seekers and companies while putting a dent into CAC. Through this, we intend to deliver unique value that only the WILL Group can provide.

For example…

In I: Interesting, we enhance engagement through event planning, management services, etc.

In L: Learning, we improve skills through certification support services, training programs, etc.

In L: Living, we improve retention rates and productivity through employee benefit services linked to live events, health support services, etc.

By expanding into these business domains, we create connections through interesting opportunities, promote growth through learning, and achieve stability in the foundation of daily life, thereby further enhancing the appeal of work. As a result, working people tend to stay longer and develop more autonomous careers, while companies achieve optimized recruitment and retention costs and improved productivity.

This virtuous cycle maximizes LTV for both individuals and companies and optimizes CAC, leading to value proposition unique to the Group. By linking W with I/L/L to drive impact on LTV and CAC, we enhance our market value as a “Chance-Making Company.”

So, what initiatives will we undertake under the Medium-term Management Plan (WILL-being 2029) as we transition from “W Group” to “WILL Group”?

As previously mentioned, the core of the “WILL Group” remains Working Business. Therefore, this Medium-term Management Plan places strong emphasis on evolving Working Business into an even more robust revenue base.

In the Domestic Working Business, the strategic theme is “Expansion of talent solutions business for permanent employee and foreign workers.” The Company aims to achieve scalable and repeatable profit growth by further strengthening permanent employee staffing/outsourcing and foreign talent management services, for which investment effectiveness was validated under the previous Medium-Term Management Plan, as well as permanent placement, which was established as a new growth option, while focusing primarily on essential domains*1. Additionally, by utilizing the recruitment, placement, and retention know-how cultivated in temporary staffing, the Company will shift to domains with higher expected profitability and growth potential, thereby promoting the strengthening of the earnings structure across the Group.

*1 Domains that are indispensable for maintaining social life and are less likely to be replaced or automated by AI. These generally include domains associated with essential workers.

In the Overseas Working Business, the strategic theme is “Strengthen profitability with a focus on productivity.” The Company will promote productivity improvements while leveraging its existing customer base and expertise to establish a stable earnings base. In addition, the Company will maintain disciplined earnings management while taking into account risks related to foreign exchange fluctuations and policy changes, and will explore medium- to long-term growth opportunities by evaluating market potential and profitability for expansion into other countries and entry into new domains. By strengthening profitability that is not easily impacted by changes in market conditions, the Company aims to return to the stable profit levels that existed prior to the post-COVID surge in permanent placement demand.

Under this Medium-Term Management Plan, the Company aims to further strengthen its earnings model and achieve further profit growth based on the achievements obtained under the previous Medium-Term Management Plan, including “achieving profitability in the construction management engineer domain,”“validating the effectiveness of investments in permanent employee staffing/outsourcing and foreign talent management services,” “establishing permanent placement operations,” and “improving productivity in the Overseas Working Business.”

To meet the expectations of our shareholders, we will devote our full efforts to achieving sustainable growth and enhancing corporate value into the future. And in this, we ask for your continued support and guidance.

Medium-Term

Management Plan